New £5,000 deposit mortgages aimed at first-time buyers have reopened one of the most important debates in the UK housing market: whether expanding access to home ownership through very high loan-to-value borrowing helps first-time buyers, or whether it increases financial fragility at a difficult point in the economic cycle.

Lloyds Banking Group has launched a new low-deposit mortgage through its Halifax brand, offering first-time buyers a route onto the property ladder with a minimum deposit of £5,000, up to 98% loan-to-value, on homes worth up to £300,000, with a five-year fixed rate and no product fees. Accord Mortgages, part of Yorkshire Building Society, offers a similar £5,000 deposit mortgage up to 99% LTV on eligible properties, while Newcastle Building Society also provides a First Step mortgage up to 98% LTV. Skipton Building Society also offers a 100% LTV Track Record mortgage, but it follows a different affordability model linked to proven rental payment history, requiring eligible renters to show that rent has been paid for 12 consecutive months within the last 18 months, with household bill evidence also potentially requested.

For buyers who can afford monthly repayments but struggle to save a large deposit, these products can look attractive. They can also support activity across the wider housing chain, including estate agents, conveyancers, surveyors, removal firms, furniture retailers and local trades.

The concern is the level of leverage being introduced into the market.

Why £5,000 Deposit Mortgages Are Attractive to First-Time Buyers

The deposit barrier has become one of the hardest obstacles for first-time buyers. In many parts of the UK, rent, bills, food costs, transport and general living costs absorb the income that would otherwise be saved towards a deposit. A borrower may be able to afford a monthly mortgage payment yet still struggle to build a 10% or 15% deposit.

A £5,000 deposit mortgage changes that calculation. It allows some buyers to enter the market years earlier than they otherwise could. It may also help renters who do not have access to family support, gifted deposits or inherited wealth.

That makes the product commercially and politically attractive. It widens access to home ownership and creates an apparent answer to one of the most visible problems in the UK housing market. The risk for borrowers sits in what happens after completion.

Why Sub-£300,000 Homes Could See a Short-Term Demand Surge

Low-deposit mortgage products are likely to have the strongest effect at the lower end of the housing market, especially where eligibility is linked to property value caps. Lloyds’ Halifax product applies to homes worth up to £300,000, while Newcastle’s First Step mortgage applies to properties up to £350,000. This naturally directs more first-time buyer demand towards lower-ticket homes.

That could create a short-term boost in the sub-£300,000 market. A property that may previously have attracted buyers at £225,000 could face additional demand from renters who can now buy with a £5,000 deposit, potentially pushing the price closer to £250,000. A £250,000 property could move towards £275,000 if enough newly eligible buyers are competing for the same stock. In supply-constrained areas, the effect could be sharper because the mortgage product increases buyer eligibility faster than new housing supply can respond.

This may benefit sellers, estate agents, conveyancers, surveyors and local property-linked investors in the short term. It may also make the market feel more active, particularly in towns where lower-value housing stock is limited and first-time buyers are competing against investors, downsizers and other owner-occupiers.

The risk is that a demand-led price uplift can reverse if the wider economy weakens. If unemployment rises, mortgage arrears increase and forced sales appear, the same lower-ticket properties that rose quickly due to expanded borrowing access could fall back towards their pre-surge levels. A home bought for £250,000 after a low-deposit mortgage-driven price rise may be more vulnerable if its underlying market value was closer to £225,000 before demand expanded.

For a borrower using a 98%, 99% or 100% LTV mortgage, that matters. A fall back to the earlier market level could be enough to push the borrower into negative equity, even without a full housing crash. If a £250,000 property falls to £225,000, the asset has lost 10% of its value. A buyer who entered with a £5,000 deposit may have little or no equity left after selling costs, legal fees, early repayment charges or arrears are included.

This is why the lower-ticket market could become both the immediate beneficiary and the first stress point. The product may increase access, support transactions and lift prices in the short term, while also increasing the number of borrowers exposed if the market turns.

The Negative Equity Risk in 98%, 99% and 100% LTV Mortgages

A buyer using a 98%, 99% or 100% LTV mortgage has almost no equity cushion at the point of purchase. If the property falls in value shortly after completion, the borrower can move into negative equity quickly. The risk is greater where the purchase price has already been pushed up by a wave of newly eligible buyers.

Negative equity becomes most serious when the borrower needs to sell. If the mortgage balance is higher than the sale price, the sale proceeds will not clear the debt. That can leave the borrower unable to move without bringing cash to completion, agreeing a repayment plan with the lender, or carrying a mortgage shortfall after the property has been sold. MoneyHelper explains that negative equity can make it harder to move home or secure a new mortgage deal, while its mortgage arrears guidance states that if a home sells for less than the mortgage balance, the borrower remains responsible for the shortfall.

That is the real risk for low-deposit borrowers. A buyer may be able to afford the mortgage at the point of completion, but if they lose their job, separate from a partner, become ill, need to relocate, or face higher refinancing costs, they may need to sell at exactly the wrong time. If the property has fallen in value, selling may crystallise the loss and leave them with debt after the home has gone.

For example, a buyer who purchases at £250,000 with a £5,000 deposit may borrow around £245,000 before fees and costs. If the property later falls to £225,000, the sale proceeds may be around £20,000 below the mortgage balance before arrears, legal fees, estate agency costs, early repayment charges or lender costs are considered. The borrower may no longer own the property, but they may still owe the lender money.

The same problem becomes larger at higher values. On a £300,000 property, a 98% mortgage would mean borrowing around £294,000, while a 99% mortgage would mean borrowing around £297,000. If that property falls to £270,000, the borrower may already be tens of thousands of pounds short before transaction costs are included. If the property falls further, the shortfall widens.

This can trap borrowers in several ways. They may be unable to sell because the lender will not release its charge unless the shortfall is dealt with. They may be unable to remortgage onto a competitive product because the loan-to-value is too high. They may be forced onto a more expensive rate if refinancing options narrow. If arrears build and the property is repossessed, the borrower can still be pursued for the remaining mortgage shortfall after sale, with additional costs potentially added. Lenders may contact borrowers after a repossessed property is sold if the sale has not cleared the debt, and may take recovery action or pass the debt to a debt recovery company.

This is the central risk with ultra-high-LTV borrowing. The danger is not simply that a house price chart moves down by 10%, 20% or 30%. The danger is that a borrower with almost no equity may lose the ability to move, refinance or exit cleanly at the exact moment their personal finances are under pressure. A mortgage that passed affordability at completion can become much harder to manage if falling property values, job loss and forced sale risk arrive together.

UK Housing Shortage Does Not Remove Downside Risk

There is a reasonable argument that Britain’s housing shortage provides support for property values. If supply remains constrained and more buyers become eligible for mortgages, demand for lower-value homes may increase, especially in the sub-£300,000 market where these low-deposit products are targeted. That does not, however, make house prices immune to correction.

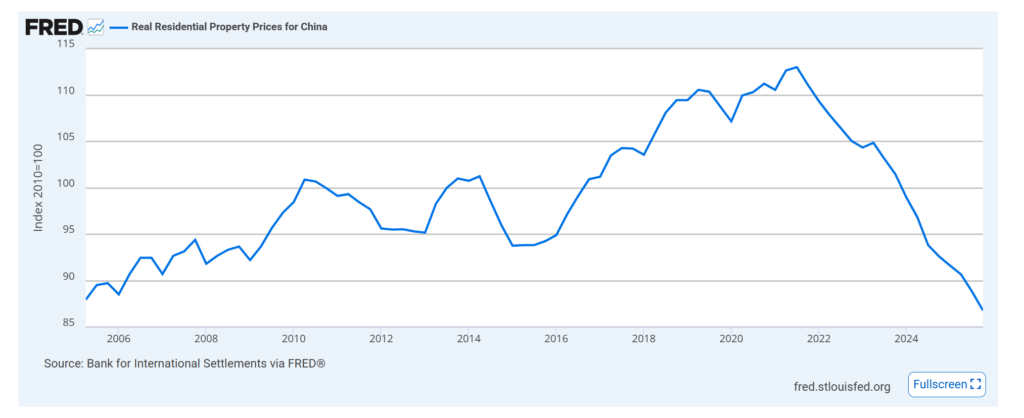

Property markets can fall even in large economies. The FRED chart below, sourced from Bank for International Settlements data, shows China’s real residential property price index falling back below its 2010 index level. China is not the UK, and the causes of China’s property downturn are different, yet the chart is a useful reminder that residential property is not a one-way asset class.

The UK has its own structural dynamics, including restricted housing supply, planning constraints, regional demand imbalances and high rental pressure. Those factors may support prices in some areas, but they do not remove the need for borrowers and lenders to stress-test downside scenarios.

The 2008 Comparison

The pre-2008 mortgage boom remains relevant because it shows how housing, employment, credit availability and consumer confidence can move together during a downturn.

The UK mortgage market is more tightly regulated today than it was before the financial crisis. Affordability checks are stronger, lender capital rules are different, and the market is not identical to the conditions seen before 2008.

Even so, the economic sequence is worth remembering. When property prices fall, highly leveraged borrowers lose flexibility first. If unemployment rises at the same time, some households may need to sell into a weaker market. If they are in negative equity, selling may not clear the debt.

That is where high-LTV products become economically sensitive. The risk is not the existence of a £5,000 deposit mortgage by itself. The risk is what happens if many households enter the market with minimal equity at a time when recession fears, cost pressures and business stress are already rising.

Why Recession Fears Matter to the Mortgage Debate

The IWOCA SME Expert Index shows that 54% of surveyed brokers said their SME clients were concerned or very concerned about recession, up from 35% in 2024. The data is based on a quarterly survey of UK finance brokers who collectively submit thousands of small business finance applications each month.

The relevance to high-LTV mortgages is the employment chain. Mortgage affordability depends on stable household income, and household income depends on businesses having enough demand, confidence and cashflow to keep staff employed. If businesses are already reporting weaker confidence, rising costs or concerns about recession, that can translate into delayed hiring, reduced overtime, shorter shifts, cancelled investment, recruitment freezes or redundancies.

Consumer behaviour feeds into the same cycle. If households cut discretionary spending, consumer-facing businesses see weaker takings through lower bookings, reduced retail footfall, smaller order values and slower payment patterns. Those businesses then respond by protecting cash, reducing costs and becoming more cautious about expansion. In a weaker trading environment, the pressure on jobs can rise at the same time as highly leveraged mortgage borrowers have the least room for income disruption.

This is why recession concerns matter for low-deposit mortgages. A borrower using a 98%, 99% or 100% LTV product may be able to afford the payment while income is stable, but the risk profile changes if their employer cuts hours, removes bonuses, freezes pay or makes redundancies. A household with limited savings and little property equity has fewer options if income falls and the property cannot be sold without creating a shortfall.

The point is wider than business owners taking these mortgages directly. Many self-employed borrowers face stricter evidential hurdles when applying for residential mortgages, so the strongest link between SME stress and high-LTV mortgage risk is through employment, wages and consumer demand. Businesses and employees depend on each other. If businesses slow spending and consumers slow spending at the same time, the mortgage market can feel the effect through weaker job security, lower confidence and reduced household resilience.

A high-LTV mortgage product may therefore look affordable in a stable labour market while becoming much more fragile in a downturn. The borrower does not need to be a business owner for economic recession signals to matter. They only need to work for a business that becomes more cautious when demand weakens.

How High-LTV Mortgages Could Feed Through to the Wider Economy

High-LTV mortgages do not automatically create a crisis. The risk is cumulative.

A weakening economy can reduce employment confidence. Lower confidence can reduce consumer spending. Lower spending can hurt businesses. Weaker businesses may cut investment, reduce hiring or need additional funding. At the same time, homeowners with very little equity may become more cautious because they know they cannot easily sell, refinance or absorb a property value fall.

This can create a feedback loop:

- households reduce discretionary spending;

- consumer-facing businesses experience weaker demand;

- business cashflow pressure increases;

- lenders become more cautious;

- credit availability tightens;

- refinancing becomes harder;

- financially stretched borrowers have fewer exit options.

For businesses, the housing market is not separate from business conditions. It affects consumer behaviour, staff confidence, owner-manager balance sheets and lender appetite.

Why the Timing of These Products Deserves Scrutiny

The timing of high-LTV expansion deserves scrutiny because the broader economic environment is already fragile.

Businesses are dealing with higher running costs, energy price concerns, supply-chain disruption, wage pressure and tighter consumer spending. Households are still adjusting to higher interest rates than those seen during the ultra-low-rate period. Many borrowers who fixed at lower rates in earlier years have already refinanced, or will refinance, into a more expensive environment.

Introducing more very high-LTV borrowing during this period may support buyers in the short term, yet it also places more households into a position where they have limited protection against valuation shocks.

That does not mean the products should be banned. It does mean the market should avoid treating them as an uncomplicated solution to affordability.

The Policy Question: Access Versus Resilience

Helping first-time buyers onto the property ladder is a legitimate policy objective. A market where only buyers with family-backed deposits can access ownership creates long-term social and economic problems. The issue is whether access is being created through a structure that remains resilient under stress.

A low-deposit mortgage can help the right borrower buy a suitable property at a sensible price with stable income, good budgeting discipline and enough reserves to manage unexpected costs. The same product can become dangerous if it encourages borrowers to stretch to the maximum loan, buy at inflated values, rely on perfect employment stability and assume property prices will continue rising.

The policy debate should therefore focus on borrower resilience, and protection in economic downturn, not in access alone.

What First-Time Buyers Should Consider Before Taking a £5,000 Deposit Mortgage

A buyer considering taking advantage of this new £5,000 deposit mortgage should approach the decision like a stress test, not a marketing offer.

They should consider buying below their maximum affordability, keeping an emergency reserve, checking local resale demand, avoiding overpaying in a heated market, and modelling future payments at a higher interest rate than the initial fixed rate.

They should also be cautious about using the entire savings pot as the deposit. A homeowner with no emergency reserve may be more exposed than a renter with cash savings, especially once repairs, insurance, service charges, furniture, moving costs and maintenance are included.

The right property also matters. A well-located home with broad resale demand may be less risky than a niche property, a new-build premium unit, a flat with service charge uncertainty or a home in an area with thin buyer demand.

How to Borrow Safely With a £5,000 Deposit Mortgage

A £5,000 deposit mortgage should be approached as a high-leverage financial decision, even where the monthly payment appears affordable. The safest borrower is not necessarily the one who can borrow the maximum amount offered by the lender. The safer borrower is the one who keeps enough margin to survive a bad sequence of events.

The first step is to avoid borrowing at the absolute top of your affordability threshold. If a lender is prepared to offer a certain maximum loan, that does not automatically mean the borrower should take it. A household that buys below its maximum borrowing capacity has more flexibility if income falls, bills rise, repairs are needed, or mortgage rates are higher at the next refinance.

Borrowers should also stress-test the payment against realistic disruption. A useful test is whether the mortgage could still be paid if it took three to six months to find another job. This matters because redundancy rarely arrives alone. It can coincide with reduced savings, higher credit card use, delayed benefit payments, relocation costs or the need to accept a lower-paid role.

A borrower should ask:

- Could I pay the mortgage for three to six months if I lost my job?

- Would I still be comfortable if my next mortgage rate was 1% to 2% higher?

- Do I have an emergency fund after paying the deposit, legal fees, moving costs and furniture costs?

- Could I afford repairs, insurance, service charges or maintenance without using credit cards?

- Would I still buy the property if I had to keep it for seven to ten years?

- Could I sell the property without a major loss if prices fell by 10%?

- Am I relying on overtime, bonuses, commission or business income that could reduce in a downturn?

The strongest position is to keep a separate cash buffer after completion. A buyer who uses every available pound to complete the purchase may technically own a home, but they may have less financial resilience than they had as a renter. Home ownership brings additional costs that renters often underestimate, including maintenance, repairs, insurance, furniture, council tax changes, service charges and unexpected building issues.

Property selection also matters. A low-deposit borrower should be especially careful about overpaying for a property with limited resale demand. Homes with strong transport links, broad buyer appeal, sensible pricing and limited structural risk provide more protection than niche properties, high-service-charge flats, poor-quality conversions or homes in areas where demand depends heavily on a single employer.

The safest use of a low-deposit mortgage is therefore controlled borrowing, not maximum borrowing. The product can help a suitable buyer enter the market sooner, but it should be used with a margin of safety. A borrower with almost no equity at completion needs stronger cash reserves, stronger income resilience and stronger discipline than a borrower entering with a larger deposit.

Conclusion: £5,000 Deposit Mortgages Are Useful, But Risk Should Be Priced Honestly

£5,000 deposit mortgages are not inherently reckless. Used carefully, they can help creditworthy first-time buyers overcome the deposit barrier and access home ownership sooner. They may also support housing market activity and benefit the wider chain of businesses connected to property transactions.

The risk is that high-LTV lending in general concentrates exposure among borrowers with the thinnest equity buffers. If the economy weakens, house prices soften and employment conditions deteriorate, some borrowers may find that the product that helped them enter the market also leaves them with limited exit options.

The more balanced conclusion is that low-deposit mortgages can be useful, yet they should be treated as higher-risk borrowing. Borrowers, lenders and policymakers should assess them against adverse scenarios, not against the assumption that house prices will keep rising.

For SMEs, the housing market remains relevant because household confidence, owner-manager leverage, consumer spending and lender appetite all feed into business conditions.

Speak to Finspire Finance

Speak to Finspire Finance if your business is reviewing funding, refinancing or cashflow options during a volatile credit cycle. A well-structured facility should be assessed against downside scenarios, not selected on headline access alone.