Most business owners don’t struggle with Self Assessment because they don’t understand it. By the time January arrives, the calculation has usually been done, the liability confirmed, and the number accepted. What causes frustration is not complexity, but disruption.

Self Assessment forces a large personal tax payment at a moment when cash is least idle. The weeks after Christmas are typically quiet, margins are thinner, and attention is already focused on restarting growth for the year ahead. Removing a substantial lump sum from circulation at that point rarely aligns with how a business actually operates.

That mismatch between tax timing and commercial reality is why Self Assessment remains one of the most resented obligations for SME owners, even when the business itself is profitable.

The Opportunity Cost Nobody Talks About

The money used to settle Self Assessment is rarely surplus capital. In most cases, it already has a purpose. It is working capital that would otherwise be used to support staff, fund marketing, place supplier orders, invest in systems, or simply provide a buffer against uncertainty.

When that cash is diverted to HMRC in one payment, the cost is not just the tax itself. It is the lost opportunity to deploy that capital productively over the following months. Businesses often end up compensating later by leaning on overdrafts, delaying investment, or taking more expensive forms of credit to restart momentum.

From a commercial perspective, this is inefficient. It is not that the tax is unfair; it is that the payment structure is blunt.

The Cashflow Gap Self Assessment Creates

Self Assessment creates a temporary but very real imbalance. The liability must be settled immediately, yet the benefit of retaining that cash would have been realised gradually over the year. That gap is where stress, hesitation, and reactive decisions tend to appear.

This is not about avoiding tax, deferring tax, or negotiating with HMRC. The obligation is clear and non-negotiable. The only question is whether the business owner absorbs the full cashflow impact in one moment, or manages it in a way that aligns with how their business actually generates value.

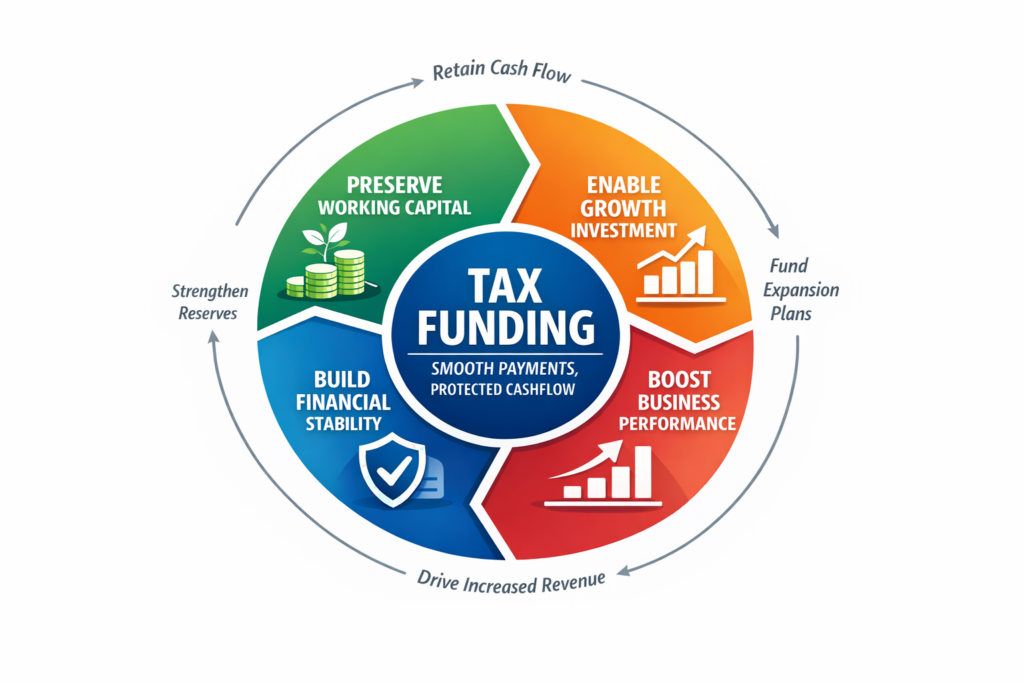

Where Tax Funding Fits

Tax funding exists to bridge that timing gap. It allows the tax to be settled on time while spreading the cost over a defined period, typically six to twelve months. Instead of Self Assessment being a disruptive event, it becomes a manageable monthly outgoing.

In practice, the structure is deliberately simple. Once the liability is confirmed, funding is arranged and the tax is either paid directly or reimbursed, depending on the circumstances. The business owner then repays the funding in fixed instalments, removing the need for a single, destabilising cash outflow.

Used properly, this does not weaken a business. It often does the opposite by preserving liquidity at a point when flexibility matters most.

How To Get Tax Funding In Place

Putting tax funding in place is intentionally straightforward. The objective is speed, certainty, and minimal disruption to the business.

1. Confirm the tax liability

You tell us the amount you need to fund. This is usually supported by an HMRC statement or confirmation from your accountant.

2. Provide recent financial information

We’ll ask for six months of business bank statements and your latest filed accounts. In some cases, up-to-date management accounts may also be required. There are no forecasts, projections, or business plans involved; the assessment is based on what the business is already doing, not what it might do.

3. We arrange the funding

Where the case is straightforward, and credit profile is clean, offers can often be secured the same day.

4. Funding is completed

Once approved, the funding is put in place and either paid directly to HMRC or to your business account. Repayments are then spread over the agreed term, typically 12 months, turning a single disruptive payment into a predictable monthly outgoing.

For many businesses, the entire process, from first conversation to funds being available, can be completed within 24 hours.

A More Financially Literate Way to Think About Self Assessment

The mistake many owners make is treating Self Assessment as a once-a-year ordeal rather than a planning decision. The tax is unavoidable, but the disruption is optional.

The more useful question is not whether the tax can be paid, but what the business could do if that capital remained in circulation. In many cases, the return on keeping that cash working comfortably exceeds the cost of spreading the payment.

That is why tax funding, when used deliberately rather than reactively, has become part of sensible cashflow management for businesses.

Contact Finspire Finance Today

Self Assessment, like all tax bills, will never feel welcome, but it doesn’t have to dictate the tone of your year. With the right structure, it can be absorbed quietly, predictably, and without compromising momentum.

For business owners who value control, that reframing makes all the difference.

If you’re approaching a Self Assessment deadline and want to spread the cost without weakening your cash position, we can assess suitability and secure funding in a matter of hours.

Your tax gets paid. Your business keeps moving.